In a constantly evolving and unpredictable world, and with numerous financial institutions competing for business, credit unions have ongoing challenges with ensuring that their members remain engaged and loyal to their credit union. These challenges will be explored and addressed in this three-part Member Engagement white paper series:

Why credit unions should care about member effort scores:

- Development of the Net Effort Score

- Is one measure of engagement sufficient? The Member Engagement Matrix

- Beyond engagement: Credit union brand love

Background

In the credit union industry, it is common for organizations to measure and track their Net Promoter Score (NPS) as a means to gauge member loyalty and potential organizational growth. It is widely adopted for its simplicity and ease of use, and credit union executives also appreciate that it enables comparisons to credit union peers and to other industries. While it is widely cautioned that organizations should not use NPS alone as their only measure of loyalty or growth (Clark and Bryan, 2013; Zaki, Kandeil, Neely, and McColl-Kennedy, 2016) (more on this to come in Issue 2 of this series), it remains one useful measure in a credit union’s toolbox.

In the past ten years, customer effort has had an influx of support as a strong measure of customer loyalty, due largely in part to the Harvard Business Review article, “Stop trying to delight your customers,” (Dixon, Freeman, and Toman, 2010) which has been followed by a variety of research efforts supporting and expanding on its claims (e.g., Clark and Bryan, 2013).

However, research has been limited in the credit union industry specifically. Furthermore, there has yet to be a consensus on how to measure customer effort. While research on NPS abounds, and studies on customer effort are growing, one area of research that is largely absent in the literature, and especially for the credit union industry, is whether there is a relationship between NPS and customer effort. A challenge that credit unions often face is knowing how to take action to change their NPS score. If customer effort has a relationship to NPS, this could be helpful in thinking about ways to take action that may influence NPS.

This white paper has three main objectives:

- Introduce the Net Effort Score (NES) as a suggested way for credit unions to measure member effort.

- Evaluate whether there is a relationship between NES and NPS.

- Provide recommendations for credit unions going forward.

Research Methodology

In 2016, in response to growing research on customer effort and to credit union clients’ desires to expand and deepen their relationships with their members, Member Intelligence Group (MIG) developed the Net Effort Score (NES). As mentioned earlier, the academic and business communities have not settled on one standard way to measure customer effort. Metrics that have been used include the Customer Effort Score (CES), which is based on a 5-point scale in response to the question, “How much effort did you personally have to put forth to handle your request?” (Dixon, Freeman, and Toman, 2010, p. 7); and the Net Easy Score, a 7- or 3-point scale based on the question, “Overall, how easy was it to get the help you wanted today?” (Clark and Bryan, 2013, p. 11). The latter has some similarities to the methodology of NPS in that it subtracts the percentage of individuals who give “difficult” scores from those who give “easy” scores (Clark and Bryan, 2013).

Building on previous research, MIG developed the NES. Research has indicated that using “easy” in the question wording is more simplistic and straightforward for customers to understand than “effort” (Clark and Bryan, 2013). Furthermore, MIG noted that previous customer effort metrics often focused on one specific experience rather than an overall impression of an organization. Given clients’ desires to gain insight on a higher level, the question, “Overall, how easy is it to do business with the credit union?” was developed. To determine the scale, MIG took a step further than the Net Easy Score with regard to using similar methodology to the NPS. It was determined that MIG’s NES methodology would fully mirror that of NPS and use the same 11-point scale and method of calculation. This would provide consistency, allow for intra- and inter-industry comparison, and be familiar and straightforward to organizations and members alike.

In the past four years, the NES score has been used with dozens of credit unions. For this current research, MIG data from twenty-three credit unions of varying asset sizes, geographical locations, and charters was accessed and studied. Data was from 2016-2019 and consisted of approximately 23,000 unique member responses to the questions utilized to calculate NPS and NES scores. Pearson correlation coefficients and r2 values were calculated in order to investigate

whether there is a linear relationship between NPS and NES.

Findings

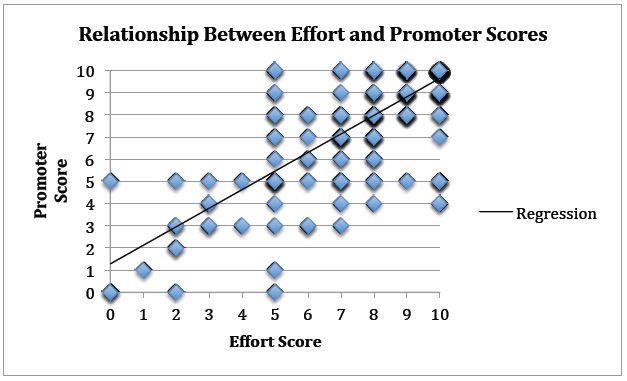

The Pearson correlation coefficient for the 23,000 member responses to the NPS question and the NES question was 0.77. The Pearson correlation coefficient range is from -1.0 to 1.0. Thus, a score of 0.77 indicates a strong positive correlation between members’ responses to the NPS question and their responses to the NES question. In other words, as one goes up, the other tends to go up as well. It is important to note that this does not indicate that one causes the other, but it does demonstrate that responses to the two questions tend to move up or down together.

The r2 value for responses to the two questions was calculated as well and was 0.60. This indicates that 60% of the variability of the responses to one question is shared by, or can be attributed to, variability of the responses to the other question, which indicates that the size of the effect of the correlation is strong. Figure 1 below shows a graphical example.

As the number of member responses varied greatly among the 23 credit unions whose data was used for this analysis, and thus in order to ensure that the behavior of one credit union’s members did not overly influence the overall correlation coefficient, a weighted average Pearson and r2 were calculated as well. These also had values of 0.77 and 0.60. Thus, it appears to not be the case that one credit union had undue influence on the results of the analysis.

Figure 1. Relationship between effort and promoter scores.

Recommendations

What do the findings mean for credit unions? Beyond the recommendation of tracking and reducing effort as one strategy to enhance loyalty, as supported in the literature (e.g., Dixon, Freeman, and Toman, 2010; Clark and Bryan, 2013), the research presented in this white paper makes new contributions to the study of member effort. Specifically, it is recommended that credit unions:

- When thinking about ways to improve NPS, consider making strides toward reducing member effort. While the current research does not claim that changes in effort will cause changes in NPS, there is a relationship between scores on the NPS question and the NES question. Reducing effort is actionable for credit unions, whereas changing promoter scores is less so. Reducing member effort will have benefits on customer loyalty on its own as well.

- When measuring member effort, utilize the NES scale. It allows for the most straightforward comparison to NPS and is most recognizable to members and credit unions alike. Issue surveys at regular intervals to monitor progress and change actions when necessary.

- Use the NES scale not only as a measure of overall member engagement but for individual transactions. Specifically, use the scale in your daily transaction surveys, new account surveys, and at other touchpoints. The question wording will change slightly (for example, “Overall, how easy is it to open an account with the credit union?), but the scale will remain the same and will allow for comparisons and tracking. This information can then be used to pinpoint areas needed for process improvement work. A credit union may discover, for example, that the process for opening an account in the branch is easy for members, but the same is not true for opening accounts online. This could lead to informed and targeted process improvement in the area of online account opening.

- With the goal of incorporating the voice of the member in initiatives to reduce effort, ask members for deeper feedback as a follow-up to their responses to the NES question. Both quantitatively and qualitatively, ask for their feedback on specific areas where doing business with the credit union requires more or less effort.

For more ideas on ways you can incorporate the Net Effort Score into your business, contact Katie Swanson, VP of Consumer Insight, at [email protected].

References

Clark, M., and Bryan, A. (2013). Customer effort: Help or hype? Henley Centre for Customer Management, April, pp. 1-22.

Dixon, M., Freeman, K., and Toman, N. (2010). Stop trying to delight your customers. Harvard Business Review, July-August, pp. 1-16.

Zaki, M., Kandeil, D., Neely, A., and McColl-Kennedy, J. R. (2016). The fallacy of the Net Promoter Score: Customer loyalty predictive model. Cambridge Service Alliance, October, pp. 1-25.